Data Mining and Text Mining project report

Mirko Mantovani, Matteo Marziali, Piervincenzo Ventrella, Stefano Cilloni

This is the report of the project of Data Mining and Text Mining course 2018 at Politecnico di Milano

in collaboration with the Bip.xTech Company.

The Goal of the project was to provide a working forecasting model given 2 years of records and for each store predict the sum of product sold for March and April 2018.

1.0 Data Analysis and Visualization (Notebook 1.0)

1.1 Intro

In this section we explored the Dataset and its structure visualizing the attributes and studying their values’ distribution and correlation.

1.2 Sales and customers distribution

We first focused on the target NumberOfSales and sequentially on NumberOfCustomers that results strongly correlated with the former.

We immediately noticed the presence of several days in which both attributes have a zero value. This is mainly due to the fact that the stores were closed in those days. This is the reason why during the preprocessing we decided to drop the instances in which the attribute ‘IsOpen’ was 0, as well as the probably erroneous rows in which the Sales and Customers are 0 even if the store is open.

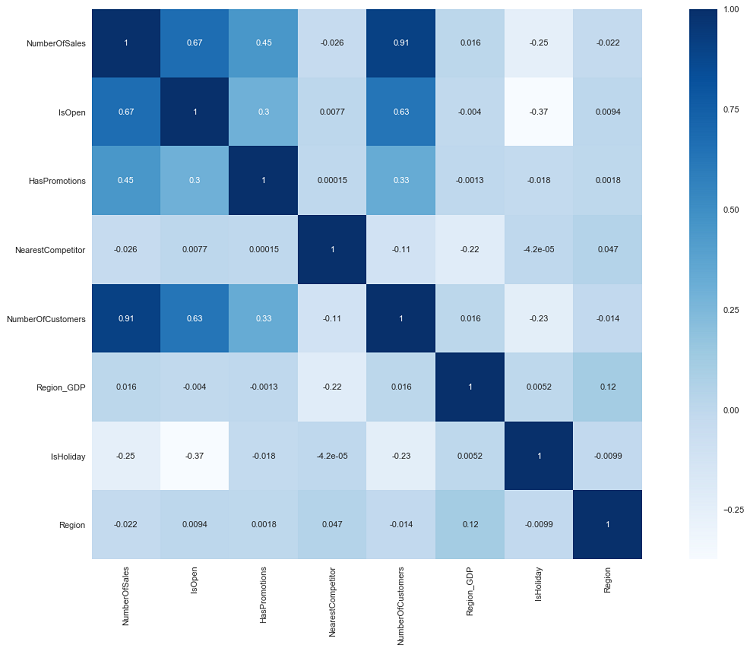

1.3 Pearson’s correlation coefficient

Since knowing the data is the starting point of any analysis, proceeded to identify the most important dependences between pairs of features, in particular, what we were interested in was the correlation or anticorrelation that the target ‘NumberOfSales’ had with the other features.

We used first the Pearson’s correlation coefficients in the Correlation Matrix to initially try to spot the variables that could influence the sales. The full details of the Dataset exploration process can be found in the notebooks of chapter 1.

.

2.0 Data preprocessing

2.1 Intro

In this section we performed a strong data preprocessing both extracting relevant attributes and performing imputation of the missing values.

Then we performed encoding of the categorical attributes. Lastly, we performed Principal Component Analysis on the attributes related on the weather condition. This choice was taken after noticing the large count of attributes related to the weather and their weak correlation with the target (so we decided to combine as many attributes as possible in order to drop them from the dataset used as a train and then obtain a less-variables better model.

The full details can be found in the notebooks of chapter 3.

2.2 Features extraction

We first extracted from the ‘Date’ attribute the attributes: ‘Day’, ‘Month’ and ‘Year’ that resulted useful for the next tasks.

Thanks to them we noticed that the volume of NumberOfSales remained constant over the years and there was no strong trend components.

The mean value of NumberOfSales calculated on each Month for each store remained quite constant with only little variations and a maximum on the Month of December.

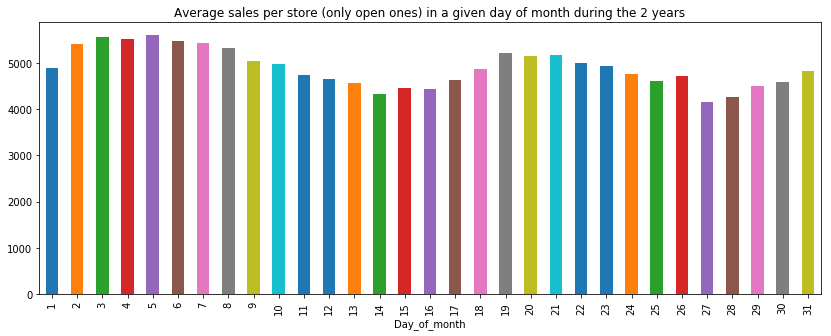

Moreover, we noticed the presence of a seasonal component during the single month, as the below diagram shows, probably due to the fact that promotions were introduced mainly at the beginning and in the middle of the month or other factors not captured from the Data. The analysis on the Dates can be found in the Notebook 4.0

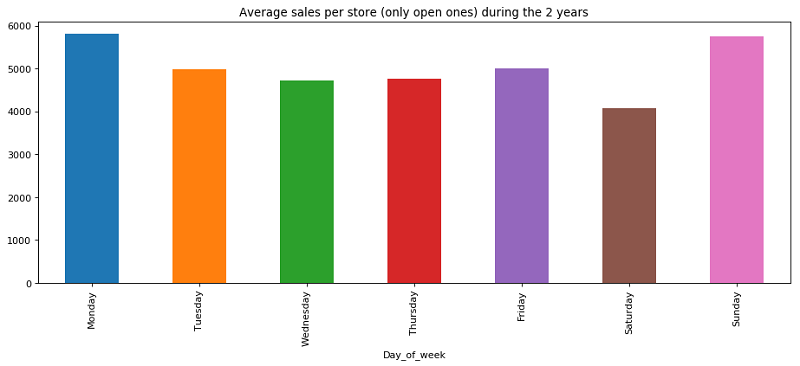

We also noticed a high variance among the day of the week.

Two other attributes that resulted important for the implementation of our model resulted in the Mean sales per Store and per Region over the 2 years of observations and the Mean Customers per store.

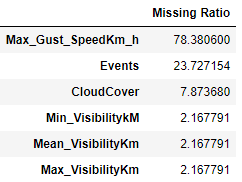

2.3 Missing Values

During this process we decided to:

-

Drop ‘Max_Gust_SpeedKm’ because of the fact of the high missing ratio and to not introduce strong Bias imputing it;

-

Impute the missing ‘Events’ with the label ‘NoEvents’;

-

Impute the missing ‘CloudCover’ with ‘0’ meaning zero level of coverage;

-

Min, Mean and Max visibility with the mode of the region in that day.

-

We then decided to drop Min and Max visibility because of their weak correlation with NumberOfSales and autocorrelation index of 1 with Mean Visibility.

2.4 Encoding of categorical attributes

During this process we decided to:

-

encode the categorical attributes ‘StoreType’ and ‘AssortmentType’ using OneHotEncoding;

-

encode the attribute Events (Rain-Snow’, ‘Snow’, ‘Rain’, ‘None’, ‘Fog-Rain’, ‘Fog-Rain-Snow’,\ ‘Fog’, ‘Rain-Thunderstorm’, …) extracting the basic attributes (Rain, Snow, Fog, None and Thunderstorm) and using them to encode the possible combinations (i.e. the categorical value ‘Fog-Rain’ become: Fog=1, Rain=1, Snow=0, None=0, Thunderstorm=0)

-

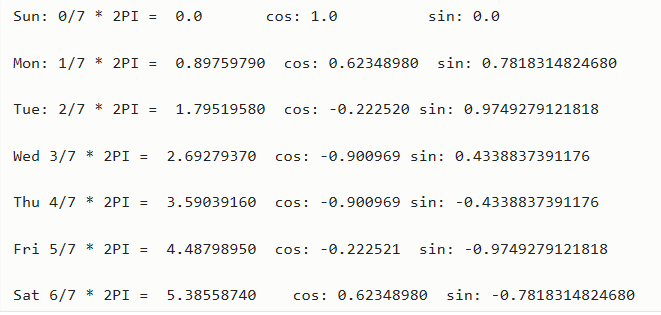

encode the day of the week (M,T,W,TH,F,S,SU) mapping them on a circumference and using the attributes sin and cos of the angle to describe them. (Initially we performed OHE but we realized that using this different encoding we obtained better performances due to the fact that with the latter we were able to encode the information of the adjacency among the days of different weeks (i.e. Monday is close both to Tuesday of the same weak and Sunday of the previous weak):

-

2.5 Principal Component Analysis

In order to reduce the number of attributes we performed principal components analysis. We decided to process all the attributes that were not much correlated with the target and to replace them in the dataset with a number of principal components that guaranteed us not to lose too much information, in terms of explained variance ratio.

In details, we processed 21 attributes through the PCA implemented by the library ‘preprocessing’ of SciKitLearn and we found out that with 12 principal components the amount of information kept was around 95.5% as you can check in the graph below. Then we created a new dataset with the principal components instead of the processed attributes.

For further details you can take a look at the notebook ‘3.4_Prepr_train_PCA’.

3.0 Baseline - how to test? (Notebook 7.2)

3.1 Baseline

The initial questions when starting the analysis were: what do we expect to achieve in terms of error? Where do we start from? What would be the results of our prediction if we had to predict right now in no more than 30 minutes and using no special algorithms? All this could be summarized in: What is a baseline for our case? Given that the error function only takes into consideration the monthly sales of a store, a good way to start drafting a prediction after having seen how the trends of sales behave over time would be to simply compute the average number of sales of each shop in the months belonging to a pair of months in a given year only considering the days in which the shop was open, and just assign to the “test set”, which is composed by the same months of the following year, the computed value, constant for each store and month. This is what was done in Notebook 7.2 by considering January and February 2017 and as test set January and February 2018. The result was a 5.3% BIP error. This does not mean we would surely achieve such an error on any month to be predicted because it was only tested on a pair of month and could have been pure luck, but it gives possible starting point that we can try to improve.

3.2 Train-test split

Initially we split train and test sets with the train_test_split in model_selection of SciKitLearn, the results were too optimistic and then we decided to split in a way that would result in having a test set similar to the one we were going to be evaluated on, so we selected some test sets a pair of months in the 24 months of the train, in particular we concentrated on the pairs that seemed more significant in our analysis based on the real test we would have had to predict in the end which are:

-

January and February 2018

-

March and April 2017

-

March and April 2016

The first one because it is the last 2 months we have and in a way this captures the real test set we have to predict, the other two were chosen because the real test set is for March and April.

4.0 Autocorrelation - lag vars (Notebook 4.1)

4.1 Intro

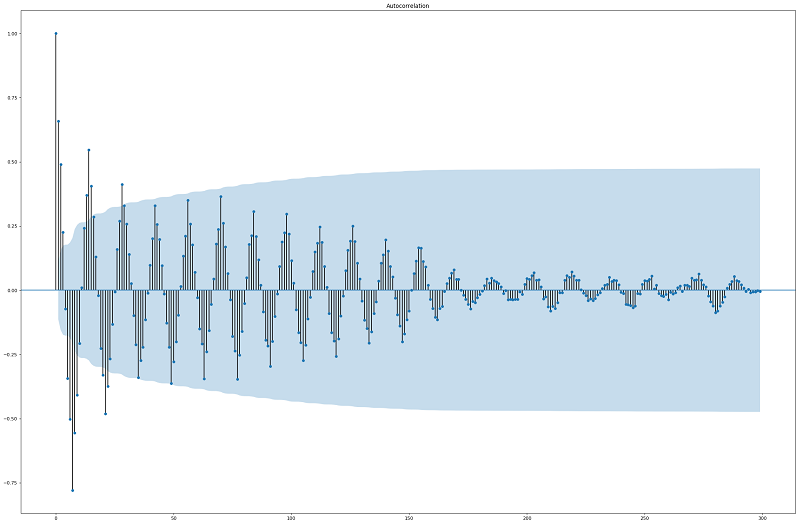

A big part of our feature engineering process was on Autocorrelation analysis and lag variables extraction. This seemed like the right direction that would lead to a better prediction since we noticed that the sales in a given day were highly correlated with the sales some of the previous days.

4.2 Correlogram

By plotting the correlogram (ACF), which shows the correlation of each

lagged observation and whether or not the correlation is statistically

significant, of the seasonality adjusted (removing seasonality and

trend) time series, we were able to discover the best lag variables to

extract, the most significant one resulted to be

7,14,1,2,9,8,6,15,21,13,20 days before the current day, we extracted all

of them and started testing the goodness of the new features on the

prediction.

4.3 The problem

When we tried to predict with the new features the results were promising, the problem was that we could not compute the lag variables on the real test set, so we tried to predict day by day and computing the lag variables on the basis of the previously predicted Sales. The overall prediction gave very bad results, and this is probably due to the fact that the training was done of “perfect” lagged sales, and they were considered by the models one of the best attributes (thus highly weighted and considered. Whereas when predicting they were only an approximation and give high importance (in practice base most of the model) to inaccurate values intuitively is not likely to lead to good performances. At that point we dropped all the attributes and completely changed direction.

5.0 Random Forest model (Notebook 5.3)

5.1 Intro

A random forest regressor is a meta estimator that fits a number of classifying decision trees on various sub-samples of the dataset and use averaging to improve the predictive accuracy and control over-fitting.

5.2 Feature selection

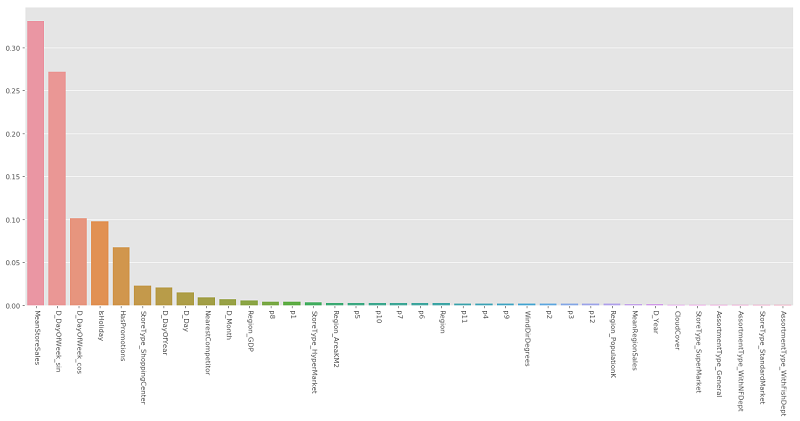

The feature selection was performed both by analyzing the feature_importances_ of the SciKitLearn’s implementation of RandomForestRegressor and by increasingly excluding the least important features that were detected by the model and plot after the training of the model

5.3 Parameters tuning

Before building the model, we tried to find effective parameters for the RandomForestRegressor by analyzing the validation curves of three main parameters: max_depth, n_estimators and max_features.

In practice, we plotted the influence of a single hyperparameter on the training score and the validation score to find out whether the estimator is more likely to lead to overfitting for some values.

5.4 Results

Different results with respect to different test sets lead us to the conclusion that RandomForestRegressor is strongly related in terms of performances to the data used to test the model.

In fact, we get very good results by testing on the bimester March-April both 2016 and 2017 or January-February 2017, but on the other hand, the BIP error computed by testing on January-February 2018 gives us terrible performances.

Such surprising outcome lead us to being stuck in choosing which results to trust more.

6.0 XGBoost model (Notebook 6.4)

6.1 Intro

eXtreme Gradient Boosting (XGBoost) is an implementation of gradient boosted decision trees designed for speed and performance. This notebook implements the final model of XGBoost used in our analysis. Since it was not easy to integrate our custom evaluation function (BIP error), we tried to minimize many built-in evaluation metrics of the XGBoost library (mae, rmse..), and then used the one that produced the best results in term of BIP error, which in this case was rmse.

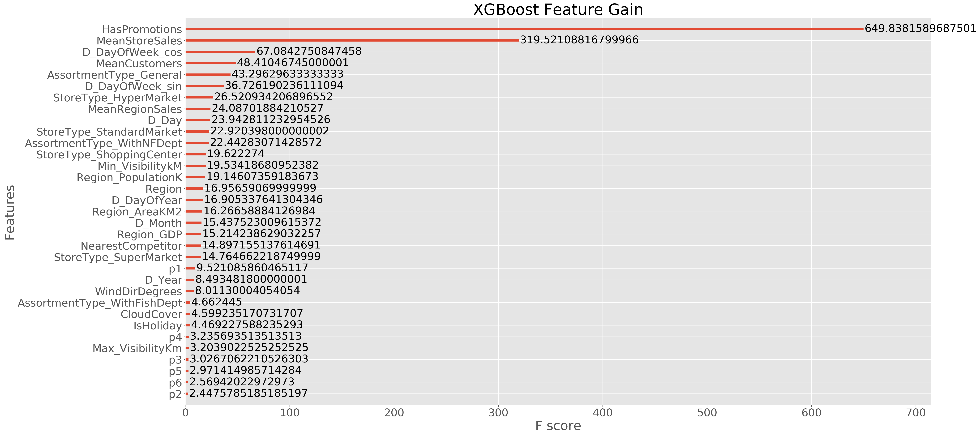

6.2 Feature selection

The feature selection was performed both by using the feature_selection

library of SciKitLearn and by increasingly excluding the least important

features that were detected by the model and plot after the training of

the model

6.3 Hyperparameters Tuning

The tuning of the Hyperparameters for XGBoost was done using the RandomizedSearchCV method and using SciKitLearn wrapper of XGBoost (XGBRegressor) with a 5-fold cross-validation on 30% of the train test and providing it the parameters: gamma, learning_rate, max_depth, reg_alpha onto which apply the Grid Search. The best parameters it found were: {‘gamma’: 14.557397447034148, ‘learning_rate’: 0.17070528151248315, ‘max_depth’: 16, ‘reg_alpha’: 11.010959407512171}, however, testing the parameters with our train-test split policy did not produce better results than the parameters found by manually try some combinations, thus, in the end we modified them.

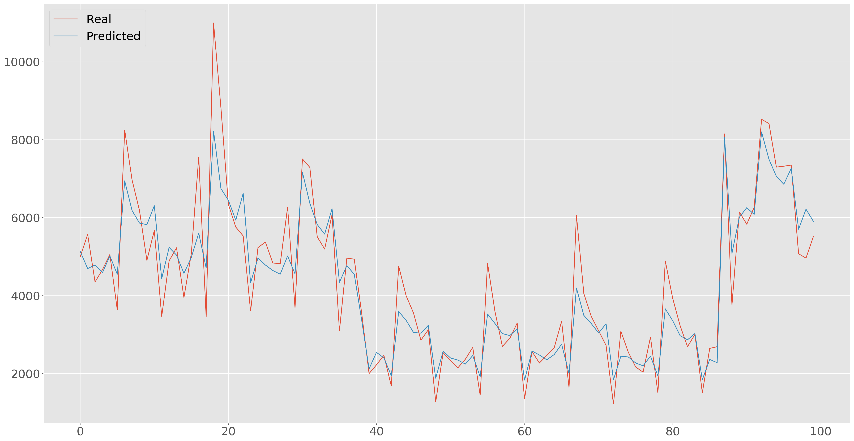

**6.4 Results **

The obtained results were promising, and even if to obtain good results

in term of BIP error we had to bring to extreme values some

hyperparameters, leading to a visible overfitting, we only cared about

having the best possible BIP

error.

We can notice that the real results has more variance with respect to the predicted ones, this is probably due to the fact that we introduced an important attribute which is the mean sales of a store, this squeezes everything and makes the prediction fall in a small range around the average sales per day, but this is what we want since we don’t want to minimize a function that takes into account errors on single days but it looks at the monthly sales.

7.0 Final Model and conclusions

7.1 Intro

The last important decision to make was which of the final models to use. Further studies were necessary to decide this.

7.2 Model comparison (Notebook 8.0)

To compare the models, we plotted the predicted number of sales for each store of different models and the real sales as bar plots. In this way we were able to see the difference in the predictions of the various models, if there were anomalous behaviors in a specific month or for some specific stores.

7.3 Random Forest – XGBoost ensemble (Notebook 7.1)

For

the final prediction, since we had already observed that one model was

better at predicting for some specific test sets, and the other for

other test sets, we decided to try average the predictions of each day

made by the two models. By doing this on some test sets the error was

almost always slightly less than the mean of the errors of the two

separate models. The final

decision was the one to use this more robust model to predict on the

real test set instead of trying to guess which of the two models could

give us the best result for, we thus reduced the risk to do choose the

worst model but also lost the chance to do maybe much better.

For

the final prediction, since we had already observed that one model was

better at predicting for some specific test sets, and the other for

other test sets, we decided to try average the predictions of each day

made by the two models. By doing this on some test sets the error was

almost always slightly less than the mean of the errors of the two

separate models. The final

decision was the one to use this more robust model to predict on the

real test set instead of trying to guess which of the two models could

give us the best result for, we thus reduced the risk to do choose the

worst model but also lost the chance to do maybe much better.